Introduction

Thousands of municipal water storage tanks across the US were built between the 1950s and 1980s — and many are still in service today. The potable water tank coating market exists to address a straightforward but high-stakes problem: keeping those aging assets safe, compliant, and functional without replacing them outright.

For facility operators, municipal engineers, and contractors, understanding where this market is heading directly shapes capital planning and coating selection decisions.

Many facilities struggle with aging water storage assets installed between the 1950s and 1980s that are now approaching end-of-service life. The combination of stricter NSF/ANSI certification requirements, evolving PFAS regulations, and mounting pressure to rehabilitate deteriorating infrastructure is forcing organizations to rethink their approach to tank maintenance and coating selection.

Key Takeaways

- The potable water tank coating market is valued at $42.84 billion in 2024, projected to reach $67.77 billion by 2032 at 5.9% CAGR

- NSF/ANSI 600 (effective January 2023) eliminated most solvent-based epoxies, driving adoption of 100% solids and polyurea systems

- The January 2028 PFAS testing deadline under NSF 61-2024 requires operators to audit and replace non-compliant fluoropolymer water-contact components before the deadline

- Rehabilitation now outpaces new construction — the EPA estimates a $625 billion drinking water infrastructure need over the next 20 years

- Asia-Pacific leads global growth through urbanization; North America drives rehabilitation demand as aging mid-century infrastructure hits replacement age

Regulatory Tightening and the Shift to NSF-Certified, Solvent-Free Coatings

NSF/ANSI/CAN 61 and its companion standard NSF 600 govern all drinking-water-contact materials in the U.S. and Canada. In January 2023, NSF 600 reduced allowable extractable solvent limits for xylene (90 µg/L), toluene (60 µg/L), and ethylbenzene (140 µg/L) — effectively removing most conventional solvent-borne epoxy linings from potable water certification eligibility.

Procurement is shifting toward coating systems that contain no solvents by design:

- 100% solids epoxy — zero VOC content, no extractable solvent residue

- Spray-applied polyurea — rapid cure, no solvent carriers

- Moisture-cure polyurethane — field-flexible, solvent-free formulations

Prior to 2023, solvent-based epoxies held a substantial share of the potable water coating market. That share is now contracting as NSF 600 compliance eliminates them from new specifications.

The PFAS Compliance Clock Is Ticking

The 2024 edition of NSF 61 introduced expanded PFAS testing requirements for fluoropolymer-containing components with a strict January 1, 2028 compliance deadline. While standard epoxy and polyurea coatings are typically unaffected, gaskets, sealants, O-rings, valve seats, and other fluoropolymer components in the water-contact zone will require updated certification.

Specification writers can no longer treat coatings in isolation. Every water-contact component — gaskets, seals, valve seats, O-rings — must be audited against updated PFAS limits. Facilities that delay this system-level review risk non-compliance when the January 2028 deadline arrives.

Eco-Friendly and Low-VOC Formulation Innovation

Environmental mandates, green building programs (LEED, BREEAM), and corporate sustainability commitments are pushing coating manufacturers toward waterborne, bio-based epoxy, and high-solids formulations. The goal: reduce volatile organic compound (VOC) emissions without sacrificing protective performance.

Bio-based epoxy resins, which partially substitute petroleum-derived components with plant-derived alternatives, are entering mainstream use. For example, PPG's AQUATAFLEX 505 is a USDA BioPreferred certified hybrid coating that meets NSF/ANSI Standard 61 for potable water tanks. Waterborne primers that meet NSF 61 certification are increasingly specified alongside 100% solids topcoats to create low-emission coating systems.

The global waterborne coatings market is projected to reach $89.35 billion by 2030, growing at 5.6% CAGR, reflecting consistent adoption across municipal and industrial procurement channels.

Why this trend is accelerating:

- Regulatory pressure from VOC emission limits at state and federal levels (SCAQMD Rule 1113 limits industrial maintenance coatings to 100 g/L)

- Procurement preferences from municipalities with published sustainability goals

- LEED v4 credit requirements for low-emitting materials

- Corporate ESG commitments driving specification changes

For specifiers and facility managers, these drivers mean low-VOC formulations are increasingly the default — not the exception — in potable water tank coating projects.

Smart Technology, AI, and Predictive Maintenance Integration

IoT-enabled sensors, AI analytics platforms, robotic coating systems, and digital twin modeling are reshaping how water tank maintenance gets managed. The shift is away from fixed replacement schedules toward condition-based decisions driven by real sensor readings.

Real-World Adoption Demonstrates ROI

AI and machine learning tools analyze corrosion progression, flag coating degradation from sensor data, and forecast recoating timelines before failures occur. Early deployments show measurable results:

- Thames Water saved 5.78 megalitres of water per day within 20 weeks using Ovarro's LeakNavigator AI acoustic monitoring system

- Qlayers' 10Q robotic coating system cuts material waste and overspray by up to 35% while reducing worker exposure to confined-space and elevated-height hazards

The business case: Tank owners and utilities managing distributed storage networks face high inspection costs and unplanned downtime risk. Predictive tools that extend coating service life and tighten maintenance scheduling directly reduce lifecycle costs — making adoption financially viable even for budget-constrained municipal operators.

Aging Infrastructure and the Growing Demand for Tank Rehabilitation

A significant portion of the world's potable water storage infrastructure — particularly steel and concrete tanks installed between the 1950s and 1980s — is approaching or exceeding its designed service life. This is creating a large and sustained market for tank rehabilitation, recoating, and relining as operators weigh the economics of repair versus full replacement.

Federal Funding Meets Massive Infrastructure Need

The EPA's 7th Drinking Water Infrastructure Needs Survey identifies a $625 billion need over the next 20 years for pipe replacement, storage tanks, and treatment plants. The Bipartisan Infrastructure Law (IIJA) directed $11.7 billion to the Drinking Water State Revolving Fund and $4 billion for emerging contaminants.

The U.S. and Canada experience approximately 260,000 water main breaks annually, costing $2.6 billion in repairs — underscoring the scale of aging infrastructure challenges.

Fusion-bonded epoxy recoating and cementitious relining of existing structures extends tank service life by 20–30 years at a fraction of replacement cost. That makes in-place restoration the economically rational choice in most mature market scenarios.

Several factors are driving municipalities and facility operators toward recoating over full replacement:

- Capital budgets remain constrained across most public water systems

- Environmental permitting for new tank construction adds time and cost

- Specialized contractors with field-applied systems — such as AmTech Tank Lining & Repair, which applies its proprietary DuraChem® 500 series and HydraStone Alkrete® cementitious lining across all 50 states — can complete work faster with less disruption than new builds

- In-place recoating avoids the downtime and logistical complexity of decommissioning and replacing a functioning asset

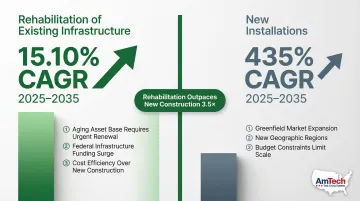

Rehabilitation of existing pipe networks in the U.S. and Canada is forecasted to grow at 15.10% CAGR between 2025 and 2035, significantly outpacing new installations (4.35% CAGR).

Hybrid and High-Performance Coating System Innovation

Hybrid coating architectures — such as an epoxy base coat paired with a polyurea or polyurethane topcoat — are seeing wider adoption in potable water tank applications. Each system type brings a distinct performance profile:

- Epoxy-polyurea hybrids: Combine epoxy's adhesion and chemical barrier properties with polyurea's flexibility and rapid cure

- Epoxy-polyurethane hybrids: Offer similar benefits with slightly slower cure, useful for larger application windows

- Glass-flake epoxy: Advancing for large-capacity steel municipal tanks where barrier thickness and permeation resistance are priorities

- Fusion-bonded epoxy (FBE): Gaining ground in high-volume steel tank applications for its consistent film build and NSF compliance

Why Hybrid Systems Solve Critical Problems

Single-component coating systems involve trade-offs between adhesion, flexibility, chemical resistance, and cure speed. Hybrid systems address these gaps directly — particularly for concrete tanks with construction joints that experience dimensional movement. Standard rigid epoxy systems cannot reliably manage that movement over multi-decade service lives, making hybrids the practical choice for engineers specifying long-term performance.

Polyurea systems offer 200-400% elongation and cure times as fast as 30 seconds, making them well-suited for concrete infrastructure subject to freeze/thaw cycles and structural movement. Rigid 100% solids epoxies, while NSF 61 compliant, are prone to micro-cracking under stress on concrete substrates.

As a result, performance-based specifications are replacing prescriptive material standards in many municipal procurement frameworks — a shift that favors contractors who can apply multiple system types and select the right one for substrate conditions.

What's Driving These Market Trends

The global potable water tank coating market was valued at $42.84 billion in 2024 and is projected to reach $67.77 billion by 2032, growing at a 5.9% CAGR. That growth is being pulled forward by a specific set of pressures: tightening regulations, water scarcity, urbanization, and accelerating material innovation.

Regulatory and Compliance Pressure

Enforcement of the Safe Drinking Water Act in the U.S., NSF/ANSI 61/600 compliance requirements, the EU Drinking Water Directive (2020/2184), and anticipated PFAS regulations are raising the baseline specification for all potable water contact materials. An ASDWA survey found that 49 U.S. states and 11 Canadian provinces require NSF 61 compliance for public water system coatings — illustrating the regulatory reach.

Water Scarcity and Urbanization

The UN estimates that over 2.2 billion people lack access to safely managed drinking water, driving massive investment in new water storage infrastructure globally, particularly across Asia-Pacific, the Middle East, and Sub-Saharan Africa. This expands the addressable market for potable water tank coatings beyond traditional North American and European demand centers. Asia-Pacific is now the fastest-growing regional market, driven by rapid urbanization and infrastructure investment.

Material Innovation and Competitive Dynamics

Coating manufacturers are responding to regulatory pressure and customer demand by investing in R&D for solvent-free, bio-based, and hybrid formulations. For contractors like AmTech Tank Lining & Repair, that shift means applying systems — including Armor Shield Tank Linings with UL-listed and NSF/ANSI-compliant credentials — where specification requirements now make certification non-negotiable rather than optional.

How These Trends Are Reshaping the Potable Water Coating Industry

These converging trends are producing measurable changes across how tank coatings are specified, applied, and maintained — with effects visible at the operational, business, and workforce levels.

Operational Impact

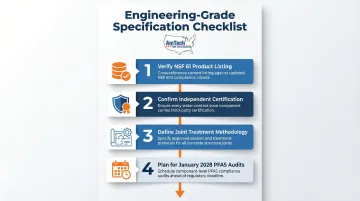

Coating selection is becoming more technically demanding. Specifiers must now:

- Verify NSF 61 product listing status against current NSF 600 criteria (not manufacturer literature)

- Confirm that every component in the water-contact zone carries independent certification

- Define joint treatment methodology for concrete structures

- Plan for January 2028 PFAS component audits

This moves procurement from a commodity purchasing exercise toward engineering-grade specification. While this increases project lead times, it reduces long-term compliance risk and prevents costly rework.

Business Impact

Regulatory-driven consolidation is reshaping competitive dynamics across the industry:

- Established certified manufacturers and experienced applicators are gaining ground over lower-cost, non-certified alternatives

- Rehabilitation and recoating contracts are growing as a share of total revenue relative to new-build work — particularly in North America and Europe

- Operators who deferred maintenance now face compressed timelines to meet updated certification requirements

Workforce Impact

Application of 100% solids and plural-component polyurea systems requires trained crews with specialized equipment:

- Plural-component spray rigs with precise ratio control

- Confined-space safety protocols and monitoring equipment

- DFT (Dry Film Thickness) verification tools

- OSHA 10/30 certification for tank entry

Growing demand against a constrained pool of certified applicators means project timelines increasingly depend on contractor availability — not just material lead times. Facilities that wait until compliance deadlines approach often find qualified crews already committed elsewhere.

Future Signals for the Potable Water Tank Coating Market

The January 2028 PFAS compliance deadline under NSF 61-2024 represents the most pressing near-term compliance trigger. Owners of water storage systems must audit all fluoropolymer-containing water-contact components — gaskets, O-rings, valve seats, and sealants — for updated certification status. This is likely to trigger a wave of component specification reviews and replacement projects beginning in 2026-2027.

Technologies to Watch

Nanotechnology-enhanced coatings offering self-healing properties and enhanced barrier performance are moving from early adoption toward mainstream specification. Nanomaterials including metal nanoparticles (nAg, ZnO, CuO) and carbon nanotubes are now being integrated by manufacturers into filtration and coating matrices for antimicrobial properties that prevent biofilm formation.

Digital twin modeling — using 3D tank models to simulate coating performance over time — is expected to become a standard pre-application engineering tool for large municipal projects. DC Water's Bentley OpenFlows WaterSight digital twin has already demonstrated value in mitigating service disruptions and reducing nonrevenue water losses.

IoT sensor integration directly into tank systems will enable real-time monitoring of coating integrity, water quality parameters, and structural conditions.

The Next 2-3 Years

Several forces are converging to drive growth in the rehabilitation segment of this market:

- NSF 600 compliance requirements remaining in full force across municipal systems

- Robotic application technology becoming more commercially accessible to mid-size projects

- Federal and state water infrastructure funding continuing to flow to aging systems

Together, these factors make potable water tank rehabilitation one of the fastest-growing sub-segments globally. Operators who begin vetting certified, technically qualified installation contractors now — before compliance deadlines force emergency decisions — will be better prepared to manage both the capital and scheduling demands ahead.

Conclusion

The potable water tank coating market is being reshaped by four converging forces: tightening regulations, aging infrastructure, sustainability pressure, and rapid coating technology advances. Together, they're driving a higher standard for what compliant, long-lasting tank protection actually requires.

Organizations that move proactively stand to gain on both compliance and cost. Three steps make the biggest difference:

- Audit existing specs against current NSF 61/600 requirements before the next inspection cycle

- Run the rehabilitation math — relining an aging tank typically costs a fraction of full replacement

- Engage NSF-certified applicators with documented field experience on potable water systems

Contractors like AmTech Tank Lining & Repair — with 55+ years of NSF-compliant field work across municipal, commercial, and industrial sites — illustrate what that expertise looks like in practice. Acting early extends asset life and keeps water systems reliably operational well into the future.

Frequently Asked Questions

What is the best material for a potable water storage tank?

The best material depends on application, capacity, and environmental conditions. HDPE works well for residential/small commercial applications, steel with certified coatings suits large municipal/industrial installations, and fiberglass excels in corrosive or underground environments. NSF/ANSI 61 certification is the baseline requirement for all potable water contact materials in the U.S.

What type of coating or paint should be used for potable water tanks to prevent corrosion?

100% solids epoxy and spray-applied polyurea are the leading NSF/ANSI 61-compliant options in 2025, as traditional solvent-based epoxies no longer meet the updated NSF 600 extractable solvent limits effective January 2023. Fusion-bonded epoxy is preferred for large steel municipal tanks, while polyurea offers faster cure times and flexibility advantages for concrete structures.

How often should potable water tank coatings be inspected or reapplied?

Most operators schedule inspections at minimum every 3-5 years, with recoating typically required every 15-25 years depending on the system and service conditions. Addressing early signs of degradation costs far less than emergency repairs or full replacement.

What certifications are required for potable water tank coatings?

In the U.S., NSF/ANSI 61 certification (in conjunction with NSF/ANSI 600 criteria) is the primary requirement for all drinking water contact materials. Certification must cover every component in the water-contact zone, not just the topcoat. The NSF product listing database should be checked for current certification status, as reformulations and delistings occur regularly.

How large is the potable water tank coating market and where is it growing fastest?

The global potable water tank coating market was valued at $42.84 billion in 2024 and is projected to reach $67.77 billion by 2032, growing at 5.9% CAGR. Asia-Pacific is the fastest-growing regional market driven by urbanization and infrastructure investment, while North America experiences strong rehabilitation-driven demand as mid-20th-century municipal water storage assets reach end of service life.

What are the main challenges facing the potable water tank coating market?

Key challenges include high initial application costs and stringent surface preparation requirements, shortage of trained certified applicators for advanced coating systems, raw material price volatility (particularly for epoxy resins), and complexity of navigating regional certification requirements — especially for new market entrants trying to meet updated NSF 600 standards.